Market Outlook December 2017

Market Outlook December 2017

As we approach 2018, it‘s time to reconcile the past 365 days of 2017. We are sending off a very exciting and tempestuous year. The stock market is at an all-time high. Volatility is at a record low. Consumer spending and confidence have passed pre-recession levels.

I would like to wish all my readers and friends a happy and prosperous 2018. I guarantee you that the coming year will be as electrifying and eventful as the previous one.

The new tax plan

The new tax plan is finally here. After heated debates and speculations, president Trump and the GOP achieved their biggest win of 2017. In late December, they introduced the largest tax overhaul in 30 years. The new plan will reduce the corporate tax rate to 21% and add significant deductions to pass-through entities. It is also estimated to add $1.5 trillion to the budget deficit in 10 years before accounting for economic growth.

The impact on the individual taxes, however, remains to be seen. The new law reduces the State and Local Tax (SALT) deductions to $10,000. Also, it limits the deductible mortgage interest for loans up to $750,000 (from $1m). The plan introduces new tax brackets and softens the marriage penalty for couples making less than $500k a year. The exact scale of changes will depend on a blend of factors including marital status, the number of dependents, state of residency, homeownership, employment versus self-employment status. While most people are expected to receive a tax-break, certain families and individuals from high tax states such as New York, New Jersey, Massachusetts, and California may see their taxes higher.

Affordable Care Act

The future of Obamacare remains uncertain. The new GOP tax bill removes the individual mandate, which is at the core of the Affordable Care Act. We hope to see a bi-partisan agreement that will address the flaws of ACA and the ever-rising cost of healthcare. However, political battles between republicans and democrats and various fractions can lead to another year of chaos in the healthcare system.

Equity Markets

The euphoria around the new corporate tax cuts will continue to drive the markets in 2018. Many US-based firms with domestic revenue will see a boost in their earnings per share due to lower taxes.

We expect the impact of the new tax law to unfold fully in the next two years. However, in the long run, the primary driver for returns will continue to be a robust business model, revenue growth, and a strong balance sheet.

Momentum

Momentum was the king of the markets in 2017. The strategy brought +38% gain in one of its best years ever. While we still believe in the merits of momentum investing, we are expecting more modest returns in 2018.

Value

Value stocks were the big laggard in 2017 with a return of 15%. While their gain is still above average historical rates, it’s substantially lower than other equity strategies. Value investing tends to come back with a big bang. In the light of the new tax bill, we believe that many value stocks will benefit from the lower corporate rate of 21%. And as S&P 500 P/E continues to hover above historical levels, we could see investors’ attention shifting to stocks with more attractive valuations.

Small Cap

With a return of 14%, small-cap stocks trailed the large and mega-cap stocks by a substantial margin. We think that their performance was negatively impacted by the instability in Washington. As most small-cap stocks derive their revenue domestically, many of them will see a boost in earnings from the lower corporate tax rate and the higher consumer income.

International Stocks

It was the first time since 2012 when International stocks (+25%) outperformed US stocks. After years of sluggish growth, bank crisis, Grexit (which did not happen), Brexit (which will probably happen), quantitative easing, and negative interest rates, the EU region and Japan are finally reporting healthy GDP growth.

It is also the first time in more than a decade that we experienced a coordinated global growth and synchronization between central banks. We hope to continue to see this trend and remain bullish on foreign markets.

Emerging Markets

If you had invested in Emerging Markets 10-years ago, you would have essentially earned zero return on your investments. Unfortunately, the last ten years were a lost decade for EM stocks. We believe that the tide is finally turning. This year emerging markets stocks brought a hefty 30% return and passed the zero mark. With their massive population under 30, growing middle class, and almost 5% annual GDP growth, EM will be the main driver of global consumption.

Fixed Income

It was a turbulent year for fixed income markets. The Fed increased its short-term interest rate three times in 2017 and promised to hike it three more times in 2018. The markets, however, did not respond positively to the higher rates. The yield curve continued to flatten in 2017. And inflation remained under the Fed target of 2%.

After a decade of low interest, the consumer and corporate indebtedness has reached record levels. While the Dodd-Frank Act imposed strict regulations on the mortgage market, there are many areas such as student and auto loans that have hit alarming levels. Our concern is that high-interest rates can trigger high default rates in those areas which can subsequently drive down the market.

Gold

2017 was the best year for gold since 2010. Gold reported 11% return and reached its lowest volatility in 10 years. The shiny metal lost its momentum in Q4 as investors and speculators shifted their attention to Bitcoin and other cryptocurrencies. In our view gold continues to be a solid long-term investment with its low correlation to equities and fixed income assets.

Real Estate

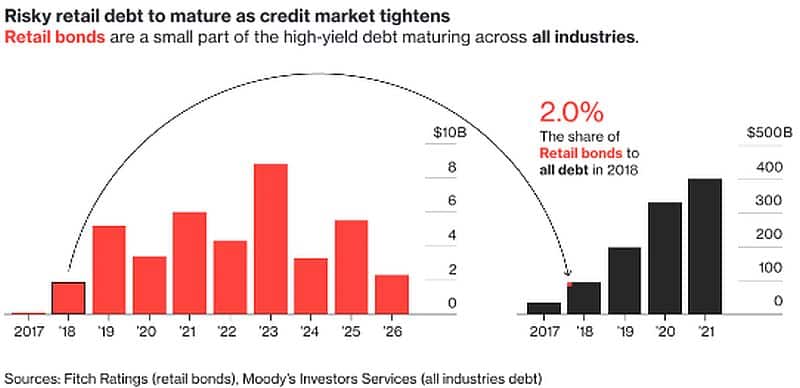

It was a tough year for REITs and real estate in general. While demand for residential housing continues to climb at a modest pace, the retail-linked real estate is suffering permanent losses due to the bankruptcies of several major retailers. This trend is driven on one side by the growing digital economy and another side by the rising interest rates and the struggle of highly-leveraged retailers to refinance their debt. Many small and mid-size retail chains were acquired by Private Equity firms in the aftermath of the 2008-2009 credit crisis. Those acquisitions were financed with low-interest rate debt, which will gradually start to mature in 2019 and peak in 2023 as the credit market continues to tighten.

In the long-run, we expect that most public retail REITs will expand and reposition themselves into the experiential economy by replacing poor performing retailers with restaurants and other forms of entertainment.

On a positive note, we believe that the new tax bill will boost the performance of many US-based real estate and pass-through entities. Under the new law, investors in pass-through entities will benefit from a further 20% deduction and a shortened depreciation schedule.

What to expect in 2018

- After passing the new tax bill, the Congress will turn its attention to other topics of its agenda – improving infrastructure, and amending entitlements. Further, we will continue to see more congressional budget deficit battles.

- Talk to your CPA and find out how the new bill will impact your taxes.

- With markets at a record high, we recommend that you take in some of your capital gains and look into diversifying your portfolio between major asset classes.

- We might see a rotation into value and small-cap. However, the market is always unpredictable and can remain such for extended periods.

- We will monitor the Treasury Yield curve. In December 2017 the spread between 10-year and 2-year treasury bonds reached a decade low at 50 bps. While not always a flattening yield has often predicted an upcoming recession.

- Index and passive investing will continue to dominate as investment talent is evermore scarce. Mega large investment managers like iShares and Vanguard will continue to drop their fees.

Happy New Year!

Final words

If you have any questions about your existing investment portfolio, reach out to me at st****@***********th.com or +925-448-9880.

You can also visit our Insights page where you can find helpful articles and resources on how to make better financial and investment decisions.

About the author:

Stoyan Panayotov, CFA is the founder and CEO of Babylon Wealth Management, a fee-only investment advisory firm based in Walnut Creek, CA. Babylon Wealth Management offers personalized wealth management and financial planning services to individuals and families. To learn more visit our Private Client Services page here. Additionally, we offer Outsourced Chief Investment Officer services to professional advisors (RIAs), family offices, endowments, defined benefit plans, and other institutional clients. To find out more visit our OCIO page here.

Contact Us