Market Outlook October 2019

Highlights:

- S&P 500 recorded a modest gain of 0.9% in the third quarter of 2019

- Ten-year treasury rate dropped to 1.5% before bouncing back to 1.75%

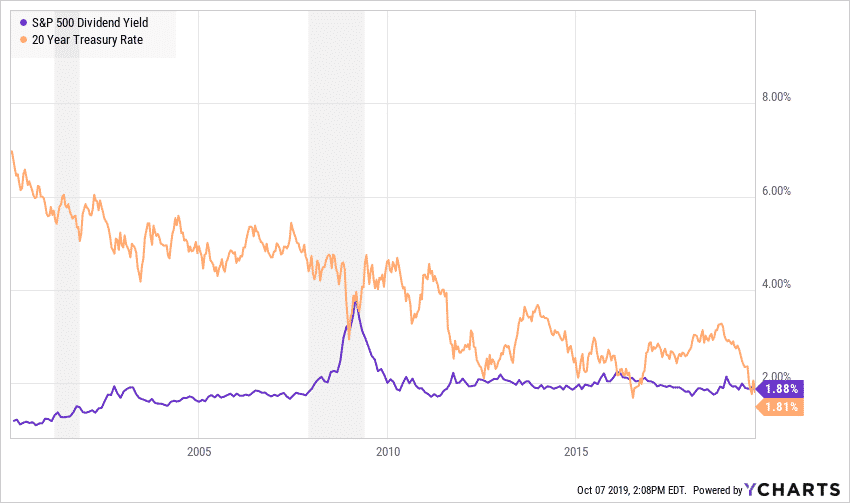

- S&P 500 dividend yield is now higher than the 20-year treasury rate

- Manufacturing index hits contraction territory

Economic Overview

- The US economy continues to show resiliency despite increased political uncertainty and lower business confidence

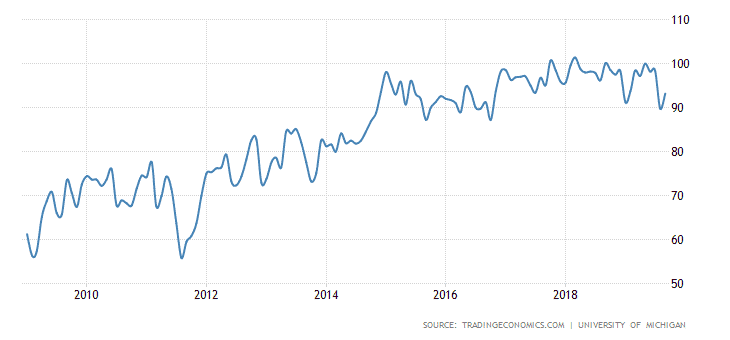

- The consumer sentiment – The US consumer is going strong. Consumer sentiment reached 93 in September 2019. While below record levels, sentiment remains above historical levels. Consumer spending, which makes up 68% of the US GDP, continues to be the primary driver of the economy.

- Unemployment hits 3.5%, the lowest level since 1969

- Wage growth of 2.9% remains above-target inflation levels

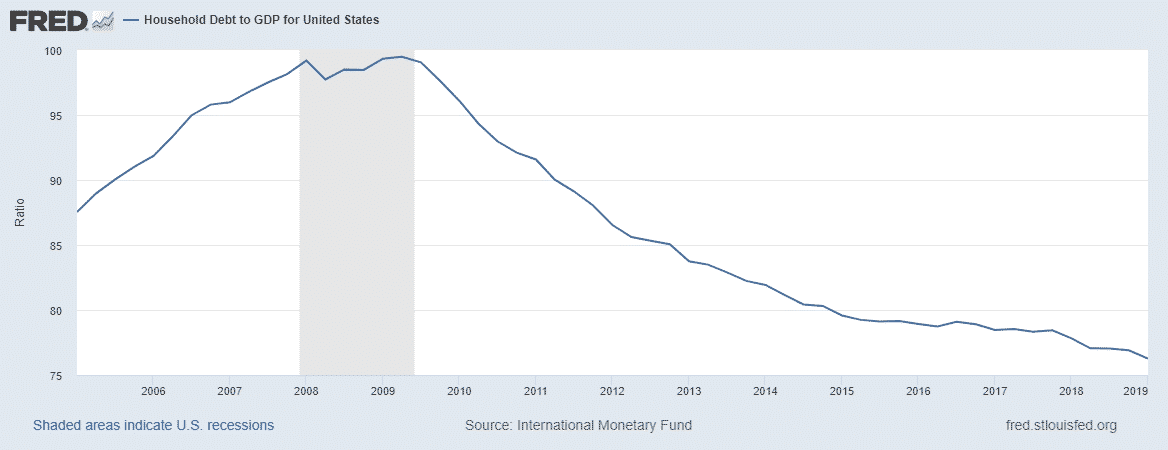

- Household debt to GDP continues to trend down and is now at 76%.

- Fed rate cuts – Fed announced two rate cuts and is expected to cut twice until the end of the year.

- The 10-year treasury rate is near 1.75%

- The 30-year mortgage rate is near 3.75%

- While low-interest rates and low unemployment continue to lift consumer confidence, the question now is, “Can the US consumer save the economy from recession’?

- The probability of recession is getting higher. Some economists assign a 25% chance of recession by the end of 2020 or 2021.

- The ISM Manufacturing index dropped to 47 in September, falling under for a second consecutive month. Typically readings under 50 show a sign of contraction and reading over 50 points to expansion. The ISM index is a gauge for business confidence and shows the willingness of corporate managers to higher more employees, buy new equipment and reinvest in their business.

- Trade war – What started as tariff threats in 2018 have turned into a full-blown trade war with China and the European Union. The Trump administration announced a series of new import tariffs for goods coming from China and the EU. China responded with yuan devaluation and more tariffs. France introduced a new digital tax that is expected to impact primary US tech giants operating in the EU.

- A study by IHS Markit’s Macroeconomic Advisers calculated that gross domestic product could be boosted by roughly 0.5% if uncertainty over trade policy ultimately dissipates.

- Chinese FX and Gold reserves – China’s reserve assets dropped by $17.0b in September, comprising of $14.7bn drop in FX reserves and a $2.4bn decline in the gold reserves. China has been adding to its gold reserves for ten straight months since December 2018.

- Political uncertainty – Impeachment inquiry and upcoming elections have dominated the news lately. Fears of political gridlock and uncertainty are elevating the risk for US businesses.

- Slowing global growth – The last few recessions were all domestically driven due to asset bubbles and high-interest rates. This time could be different, and I do not say that very often. Just two years ago, we saw a consolidated global growth with countries around the world reporting high GDP numbers. This year we witness a sharp turn and a consolidated global slowdown. EU economies are on the verge of recession. The only thing that supports the Eurozone is the negative interest rates instituted by the ECB. China reported the slowest GDP growth in decades and announced a package of fiscal spending combined with tax cuts, regulatory rollbacks, and targeted monetary easing geared to offset the effect of the trade war and lower consumer spending. So even though the US economy is stable, a prolonged slowdown of global economies could drag the US down as well.

Equities

US Equities had a volatile summer. Most indices are trading close to or below early July levels and only helped by dividends to reach a positive quarterly return. On July 27, 2019, S&P 500 closed at an all-time high of 3,025, followed by an August selloff. A mid-September rally helped S&P 500 pass 3,000 level again, followed by another selloff. S&P 500 keeps hovering near all-time highs despite increased volatility, with 3,000 remaining a distinct level of resistance.

In a small boost for equities, the dividend yield on the S&P 500 is now higher than the 10- and 20- year US Treasury rate and barely below the 30-year rate of 2%.

For many income investors equities become an alternative to generate extra income over safer instruments such as bonds

Growth versus Value

Investing in stocks with lower valuations such as price to earnings and price to book ratios has been a losing strategy in the past decade. Investors have favored tech companies with strong revenue growth often at the expense of achieving profits. They gave many of those companies a pass in exchange for a promise to become profitable in the future.

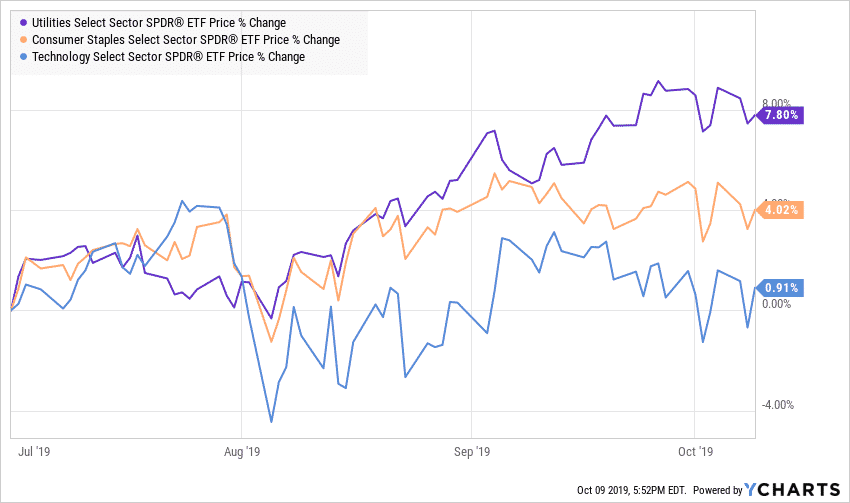

However, while economic uncertainty is going up, the investors’ appetite for risk is going down. The value trade made a big comeback over the summer as investors flee to safe stocks with higher dividends. As a result, the utilities and consumer staple companies have outperformed the tech sector.

The IPO market

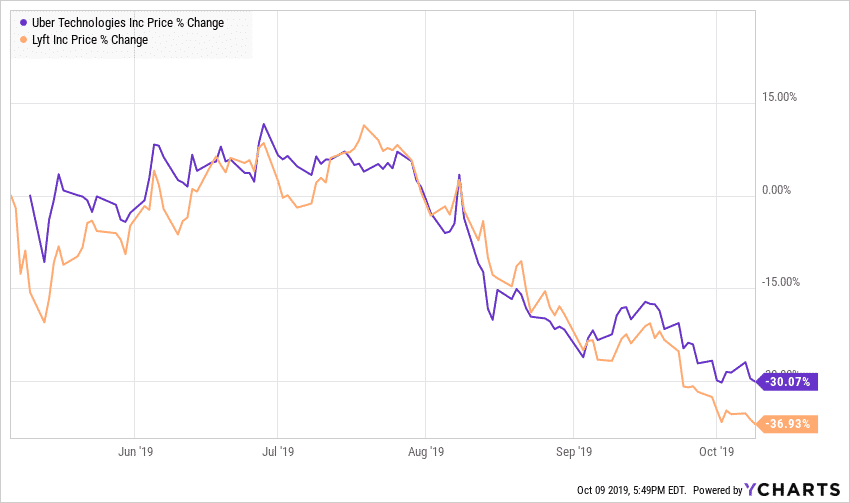

The IPO market is an indicator of the strength of the economy and the risk appetite of investors. In 2019, we had multiple flagship companies going public. Unfortunately, many of them became victims of this transition to safety. Amongst the companies with lower post IPO prices are Uber, Lyft, Smiles Direct Club, and Chewy.com. Their shares were down between -25% and -36% since their inception date. Investors walked away from many of these names looking for a clear path to profitability while moving to safety stocks.

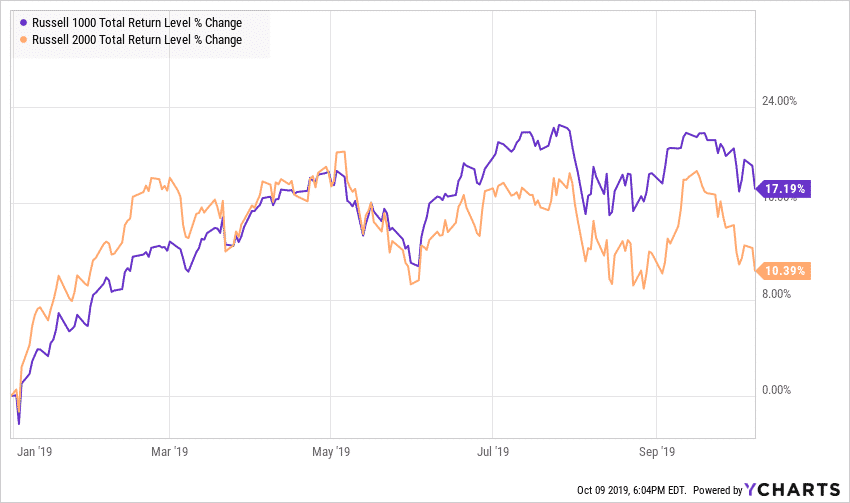

Small-Cap

Small caps have trailed large caps due to increased fears of recession and higher market volatility. Small caps tend to outperform in a risk-on environment, where investors have a positive outlook on the economy.

International Stocks

International stocks continue to underperform. On a relative basis, these stocks are better valued and provide a higher dividend than US stocks. Unfortunately, with a few exceptions, most foreign stocks have been hurt by sluggish domestic and international demand and a slowdown in manufacturing due to higher tariffs. Many international economies are much more dependent on exports than the US economy.

Fixed Income

The Fed continued its accommodative policy and lowered its fund rate twice over the summer. Simultaneously, other Central Banks around the world have been cutting their rates very aggressively.

The European Central Bank went as far as lowering its short-term funding rate to -0.50%. As a result, the 30-year German bund is now yielding -0.03%. The value of debt with negative yield reached $13 trillion worldwide including distressed issuers such as Greece, Italy, and Spain.

Investors who buy negative-yielding bonds are effectively lending the government free money.

In one of my posts earlier in 2019, I laid out the dangers of low and negative interest rates. You can read the full article here. In summary, ultra-low and negative interest rates change dramatically the landscape for investors looking to supplement their income by buying government bonds. Those investors need to take more risk in their search for income. Low rates could also encourage frivolous spending by politicians and often lead to asset bubbles.

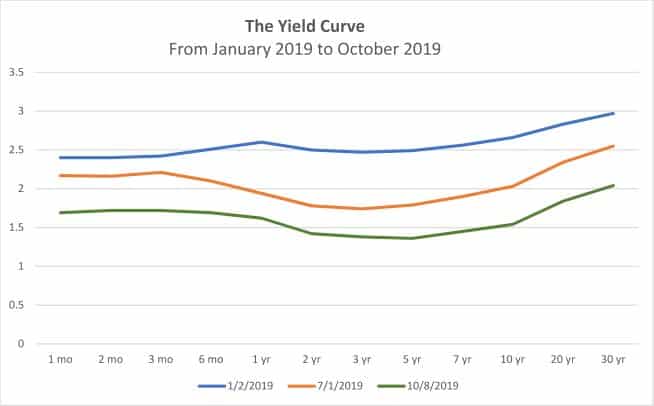

The Yield Curve

The yield curve shows what interest rate an investor will earn at various maturities. Traditionally, longer maturities require a higher interest rate as there is more risk to the creditor for getting the principal back. The case when long-term rates are lower than short-term rates is called yield inversion. Some economists believe that a yield inversion precedes a recession. However, there is an active debate about whether the difference between 10y and 2y or 10y and 3m is a more accurate indicator.

As you can see from the chart, the yield curve gradually inverted throughout the year. Short-term bonds with 3-month to maturity are now paying higher interest than the 10-year treasury

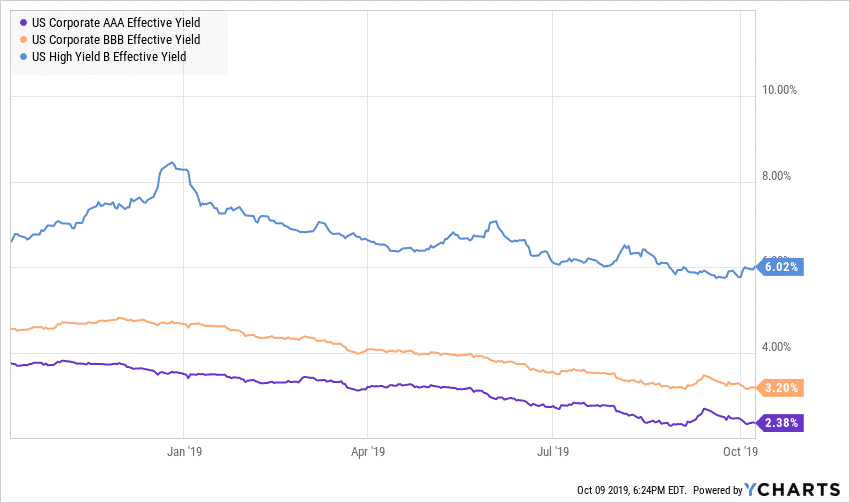

Credit spreads

The spread between AAA investment-grade and lower-rated high yield bonds is another indicator of an imminent credit crunch and possible economic slowdown.

Fortunately, corporate rates have been declining alongside treasury rates. Spreads between AAA and BBB-rated investment grade and B-rated high yield bonds have remained steady.

Repo market crisis

The repo market is where banks and money-market funds typically lend each other cash for periods as short as one night in exchange for safe collateral such as Treasuries. The repo rates surged as high as 10% in mid-September from about 2.25% amid an unexpected shortage of available cash in the financial system. For the first time in more than a decade, the Federal Reserve injected cash into the money market to pull down interest rates.

The Fed claimed that the cash shortage was due to technical factors. However, many economists link the shortages of funds as a result of the central bank’s decision to shrink the size of its securities holdings in recent years. The Fed reduced these holdings by not buying new ones when they matured, effectively taking money out of the financial system.

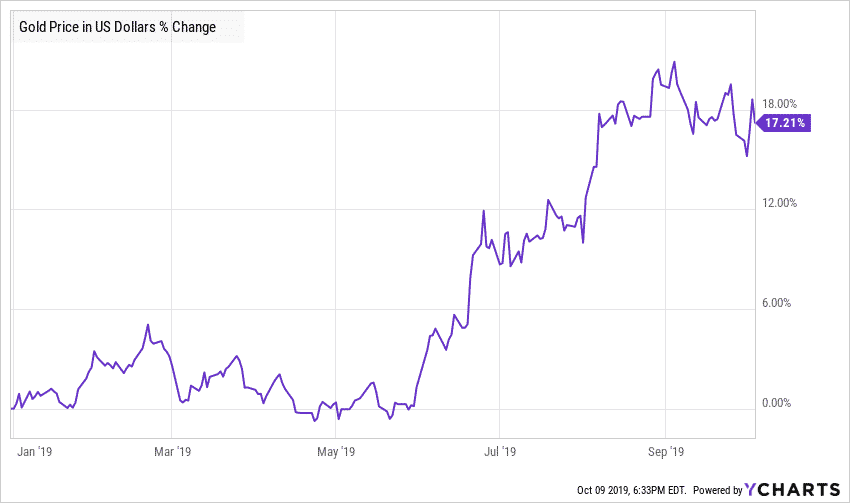

Gold

Gold has been a bright spot in our portfolio in 2019. After several years of dormant performance, investors are switching to Gold as protection from market volatility and low-interest rates. In early September, the precious metal was up nearly 21% YTD, but since then, retracted a bit.

Gold traditionally has a very low correlation to both Equities and Bonds. Even though it doesn’t generate income, it serves as an effective addition to a well-diversified portfolio.

The Gold will move higher if we continue to experience high market volatility and uncertainty on the trade war.

Final words

The US economy remains resilient with low unemployment, steadily growing wages, and strong consumer confidence. However, few cracks are starting to appear on the surface. Many manufacturers are taking a more cautious position as the effects of the global slowdown and tariffs are starting to trickle back to the US. An inverted yield curve and crunch in the repo market have raised additional concerns about the strength of the economy.

Despite the media’s prolonged crisis call, we can avoid a recession. The recent trade agreement between the US and Japan could open the gate for other bilateral trade agreements. Given that the US elections are around the corner, I believe that this administration has a high incentive to seal trade agreements with China and the EU.

The market is expecting two more Fed cuts for a total of 0.5% by the end of the year. If this happens, the Fed fund rate will drop to 1.25% – 1.5%, possibly flattening or even steepening the yield curve, which will be a positive sign for the markets.

Those with mortgage loans paying over 4% in interest may wish to consider refinancing at a lower rate.

Market volatility is inevitable. Keep a long-term view and maintain a well-diversified portfolio.

The end of the year is an excellent time to review your retirement and investment portfolio, rebalance and take advantage of any tax-loss harvesting opportunities.

About the author:

Stoyan Panayotov, CFA, MBA is the founder of Babylon Wealth Management and a fee-only financial advisor in Walnut Creek, CA, serving clients in the San Francisco Bay Area and nationally. Babylon Wealth Management specializes in financial planning and investment management for growing families, physicians, and successful business owners.

If you have any questions about the markets and your investments, reach out to me at st****@***********th.com or +1-925-448-9880.

You can also visit my Insights page, where you can find helpful articles and resources on how to make better financial and investment decisions.

Subscribe to get our newest Insights delivered right to your inbox

Latest Articles

Contact Us