Saving for college with a 529 plan

What is a 529 plan?

The 529 plan is a tax-advantaged state-sponsored investment plan, which allows parents to save for their children college expenses.

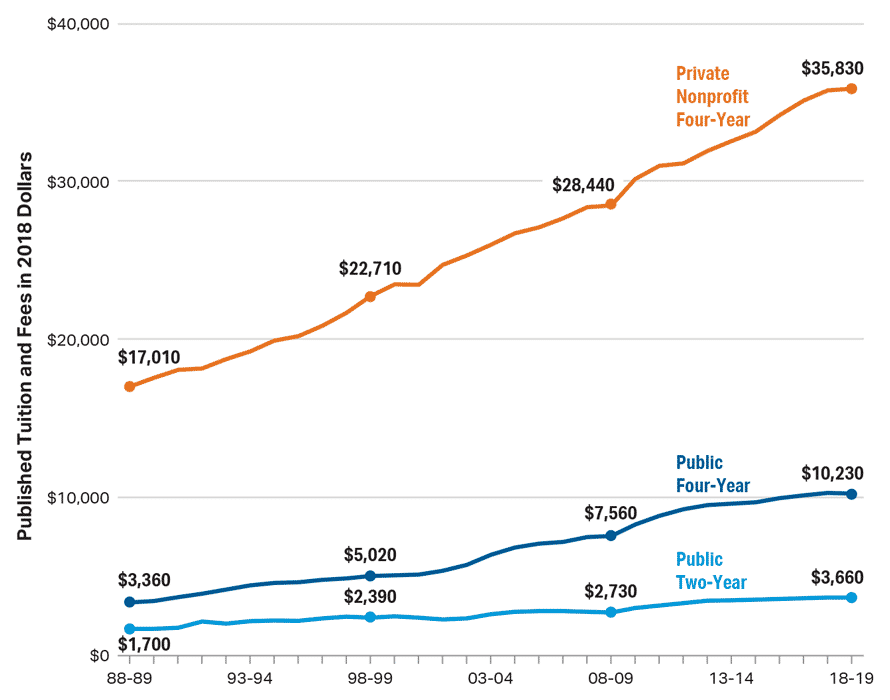

In the past 20 years, college expenses have skyrocketed exponentially putting many families in a difficult situation. Between 1998 and 2018, college tuition and fee have doubled in most private non-profit schools and more than tripled in most 4-year public colleges and universities.

With this article, I would like to share how the 529 plan can help you send your kids or grandkids to college.

Student Debt is Growing

The student debt has reached $1.56 trillion with a growing number of parents taking on student loans to pay for their children’ college expenses. The total number of US borrowers with student loan debt is now 44.7 million.

Amid this grim statistic, less than 30% of families are aware of the 529 plan. The 529 plan could be a powerful vehicle to save for college expenses. Fortunately, 529 plans have grown in popularity in the past 10 years. There are more than 13 million 529 accounts with an average size of $24,057.

Let’s break down some of the benefits of the 529 plan.

College Savings Made Easy

Nowadays, you can easily open an account with any 529 state plan in just a few minutes and manage it online. You can set up automatic contributions from your bank account. Also, many employers allow direct payroll deductions and some even offer a match. Your contributions and dividends are reinvested automatically., so you don’t have to worry about it yourself. As a parent, you can open a 529 plan with as little as $25 and contribute as low as $15 per pay period. Most direct plans have no application, sales, or maintenance fees. 529 plan is affordable even for those on a modest budget.

529 plan offers flexible Investment Options

Most 529 plans provide a wide variety of professionally managed investment portfolios including age-based, indexed, and actively-managed options. The age-based option is an all-in-one portfolio series intended for those saving for college. The allocation automatically shifts from aggressive to conservative investments as your child approaches college age.

Alternatively, you can design your portfolio choosing between a mix of actively managed and index funds, matching your risk tolerance, timeline, and investment preferences. Some 529 plans offer guaranteed options, which limit your investment risk but also cap your upside.

Earnings Grow Tax-Free

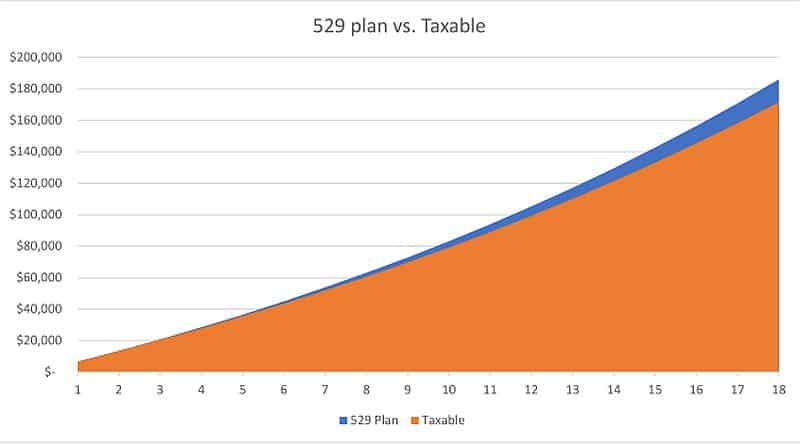

529 plan works similarly to the Roth IRA. You make post-tax contributions. And your investment earnings will grow free from federal and state income tax when used for qualified expenses. Compared to a regular brokerage account, the 529 plan has a distinct tax advantage as you will never pay taxes on your dividends and capital gains.

Tax-exempt growth

Your State May Offer a Tax Break

Over 30 states offer a full or partial tax deduction or credit on your 529 contributions. You can find the full list here. If you live in any of these states, your 529 contributions can lower significantly your state tax bill. However, these states usually require you to use the state-run 529 plan.

If you live in any of the remaining states that don’t offer any state tax deductions, such as California, you can open a 529 account in any state of your choice.

Use at Schools Anywhere

529 funds can be used at any accredited university, college or vocational school nationwide and more than 400 schools abroad. Basically, any institution eligible to participate in a federal student aid program qualifies. A 529 plan can be used to pay for tuition, certain room and board costs, computers and related technology expenses as well as fees, books, supplies, and other equipment.

The TCJA law of 2017 expanded the use of 529 funds and allowed parents to use up to $10,000 annually per student for tuition expenses at a public, private or religious elementary, middle, or high school. However, please check with your 529 plan as not all states passed that provision

Smaller Impact on Scholarship and Financial Aid

Many parents worry that 529 savings can adversely affect eligibility for scholarships and financial aid. Fortunately, 529 plan savings have no impact on merit scholarships. You can even withdraw funds from the 529 plan penalty-free up to the amount of the student scholarship.

For FAFSA, funds are typically treated as ownership of the parent, not the child, reducing the impact on financial aid application. A key component of the financial aid application is the Expected Family Contribution (EFC). Since 529 plans are considered parents’ assets, they are assessed at 5.64% of their value. For comparison, any accounts owned directly by the student such as custodial accounts (UTMAs, UGMAs), trusts and investment accounts are assessed at 20% of their value.

Lower Cost versus Borrowing Money

Starting the 529 plan early can save you money in the long run. The tax advantages of the 529 plan combined with the compounding growth over 18 years it will provide you with substantial long-term savings compared to taking a student loan.

529 plan provide Estate Tax Planning Benefits

Your 529 plan contributions may qualify for an annual gift tax exclusion of $15,000 per year for single filers and $30,000 a year for couples. The 529 plan is the only investment vehicle that allows you to contribute up to 5 years’ worth of gifts at once — for a maximum of $75,000 for a single filer and $150,000 for couples.

Other Family Members Can Contribute Too

Grandparents, as well as other family and friends, can make gifts to your 529 account. They can also set up their own 529 accounts and designate your child as a beneficiary. The grandparent-owned 529 account is not reportable on the student’s FAFSA, which is good for financial aid eligibility. However, any distributions to the student or the student’s school from a grandparent-owned 529 will be added to the student income on the following year’s FAFSA. Student income is assessed at 50%, which means if a grandparent pays $10,000 of college costs it would reduce the student’s eligibility for aid by $5,000.

Transfer funds to ABLE Account

Achieving a Better Life Experience (ABLE) account was first introduced in 2014. The ABLE account works similarly to a 529 plan with certain conditions. It allows parents of children with disabilities to save for qualified education, job training, healthcare, and living expenses.

Under the TCJA law, 529 funds can be rolled over into an ABLE account, without paying taxes or penalties.

Assign Extra Funds to Other Family Members

Finally, if your child or grandchild doesn’t need all the money or his or her education plans change, you can designate a new beneficiary penalty-free so long as they’re an eligible member of your family. Moreover, you can even use the extra funds for your personal education and learning new skills.

Contact Us