How to build your 401k plan

401k plans are a powerful savings tool for retirement

With total assets reaching $4.8 trillion dollars 401k plans are the most popular retirement vehicle and are increasingly used by employers to recruit and retain key talent. 401k accounts allow employees to build their retirement savings by investing a portion of their salary. Contributions to the plan are tax-deductible, thus reducing your taxable income, and the money allocated grows tax-free. Taxes are due upon withdrawal of funds during retirement years. In this article, I will discuss how to build your 401k plan.

Does your employer offer a 401k plan?

If you recently joined a new company, find out whether they offer a 401k plan. Some employers offer automatic enrollment, and others require individual registration.

Many companies offer a matching contribution up to a set dollar amount or percentage.

Contributions are usually deducted from each paycheck, but employees can also opt to contribute a lump sum. The 2016 limit is $18,000 plus a $6,000 “catch-up” contribution for people age 50 and above.

How to decide on your investment choices

Employers must provide ongoing education and training materials about retirement savings plans.

401k plans can offer anywhere between 5 and 20 different mutual funds which invest in various asset classes and strategies. Your choice will be limited to the funds in your plan. Hence you can not invest in stocks or other financial instruments.

The fundamental goal is to build a diversified and disciplined portfolio with your investment choices. Markets will go up and down, but your diversified portfolio will moderate your risk in times of market turmoil.

Index Funds

Index Funds are passively managed mutual funds. They track a particular index by mirroring its performance. The index funds hold the same proportion of underlying stocks as the index they follow. Many indexes are tracking large-cap, mid-cap, small-cap, international and bond indices. One of the most popular categories is the S&P 500 Index funds.

Due to their passive nature index funds are usually offered at a lower cost compared to actively managed funds. They provide broad diversification with low portfolio turnover. Index funds do not actively trade in and out of their positions and only replace stocks when their benchmark changes. Index funds are easy to buy, sell and rebalance.

Actively Managed Mutual Funds

Actively managed mutual funds are the complete opposite of index funds. A management team usually runs each fund. The mutual funds have a designated benchmark, such as the S & P 500, Russell 2000, and MSI World. Often the management team aims to beat the benchmark either by a greater absolute or risk-adjusted return. Overall active funds trade more often than index funds. Their portfolio turnover (frequency of trading) is bigger because managers take an active approach and invest in companies or bonds with the goal of beating their benchmark.

There is a broad range of funds with different strategies and asset classes. Some funds trade more actively than others. Even funds that follow the same benchmark can gravitate towards a particular sector, country or niche. For instance, a total bond fund might be more concentrated into government bonds, while another fund may invest heavily in corporate bonds.

Active funds charge higher fees than comparable index funds. These fees cover salaries, management, administrative, research, marketing, and trading costs. Funds investing in niche markets like small-cap and emerging market will have higher costs. Fees are also dependent on the size of the fund and its turnover strategy.

It’s critical to do at least a basic research before you decide which fund to purchase. Morningstar.com is a great website for mutual fund information and stats.

Target Retirement funds

These are mutual funds that invest your retirement assets according to a target allocation based on your expected year of retirement. The further away you are from retirement, the more your target fund asset allocation will lean toward equity investments. As you get closer to retirement, the portion of equity will go down and will be replaced by fixed income investments. The reason behind target retirement funds is to maintain a disciplined investment approach over time without being impacted by market trends.

One significant drawback of the retirement funds is that they assume your risk tolerance is based on your age. If you are a risk taker or risk averse, these funds may not represent your actual financial goals and willingness to take the risk.

In addition to that, investors also need to consider how target retirement funds fit within their overall investment portfolio in both taxable and tax-advantaged accounts.

Most large fund managers offer target retirement funds. However, there are some large differences between fund families. Some of the discrepancies come from the choice of active versus passive investment strategies and fees.

Without endorsing any of the two providers below I will illustrate some of the fundamental differences between Vanguard and T. Rowe Price Target Retirement funds.

Vanguard Target Retirement funds

Vanguard Target Retirement funds offer low-cost retirement fund at an expense ratio of 0.15%. All funds allocate holdings into five passively managed broadly diversified Vanguard index fund.

| Vanguard Target Retirement | 2015 | 2025 | 2035 | 2045 |

| Total Stock Market Index | 28.44 | 39.86 | 48.75 | 54.07 |

| Total Intl Stock Index | 19.01 | 26.56 | 32.45 | 35.9 |

| Total Bond Market II Index | 30.32 | 23.66 | 13.23 | 7.05 |

| Total Intl Bond Index | 13.37 | 9.92 | 5.57 | 2.98 |

| Short-Term Infl-Protected Sec Index | 8.86 | |||

| % Assets | 100.00 | 100.00 | 100.00 | 100.00 |

| By asset class | ||||

| Equity | 47.45 | 66.42 | 81.2 | 89.97 |

| Fixed Income | 52.55 | 33.58 | 18.8 | 10.03 |

T. Rowe Target Retirement funds

On the other spectrum are T. Rowe retirement funds. Their funds have a higher expense ratio. They charge between 0.65% and 0.75%. All target funds invest in active T. Rowe mutual funds in 18 different categories. T. Rowe target funds are a bit more aggressive. They have a higher allocation to equity and offer a wider range of investment strategies.

| T. Rowe Target Retirement Fund | 2015 | 2025 | 2035 | 2045 |

| New Income | 24.38 | 17.34 | 10.64 | 6.74 |

| Equity Index 500 | 22.15 | 14.85 | 9.31 | 7.41 |

| Ltd Dur Infl Focus Bd | 11.01 | 3.53 | 0.54 | 0.53 |

| International Gr & Inc | 5.04 | 6.68 | 7.85 | 8.35 |

| Overseas Stock | 5.01 | 6.64 | 7.82 | 8.3 |

| International Stock | 4.42 | 5.78 | 6.8 | 7.26 |

| Emerging Markets Bond | 3.55 | 2.47 | 1.43 | 1.01 |

| Growth Stock | 3.43 | 11.74 | 17.84 | 20.26 |

| International Bond | 3.42 | 2.44 | 1.51 | 0.98 |

| High Yield | 3.26 | 2.32 | 1.42 | 0.91 |

| Value | 3.1 | 11.31 | 17.36 | 19.75 |

| Emerging Markets Stock | 2.88 | 3.87 | 4.49 | 4.71 |

| Real Assets | 2.1 | 2.78 | 3.28 | 3.5 |

| Mid-Cap Value | 1.85 | 2.46 | 2.95 | 3.12 |

| Mid-Cap Growth | 1.78 | 2.35 | 2.73 | 2.9 |

| Small-Cap Value | 0.93 | 1.23 | 1.48 | 1.55 |

| Small-Cap Stock | 0.88 | 1.15 | 1.41 | 1.53 |

| New Horizons | 0.72 | 0.94 | 1.1 | 1.12 |

| % Assets | 100 | 100 | 100 | 100 |

| By Asset Class | ||||

| Equity | 54.29 | 71.78 | 84.42 | 89.76 |

| Fixed Income | 45.62 | 28.1 | 15.54 | 10.17 |

Which approach is better? There is no distinctive winner. It depends on your risk tolerance.

Vanguard funds have lower expense ratio and a lower 10-year return. However, they have a lower risk.

T. Rowe funds have higher absolute and risk-adjusted return but also carry more risk.

10-year Performance Analysis, 2045 Target Retirement Fund

| Standard | 10-year | Sharpe | ||

| Fund | Name | Deviation | Return | Ratio |

| VTIVX | Vanguard Target 2045 | 14.65 | 5.48 | 0.36 |

| TRRKX | T. Rowe Target 2045 | 15.82 | 5.89 | 0.38 |

*** Data provided by Morningstar

Most 401k plans will offer only one family of target funds, so you don’t have to decide between Vanguard, T. Rowe or another manager. You will have to decide whether to invest in any of them at all or put your money in the index or active funds. For further information, check out our dedicated article on target date funds

ETFs

ETFs are a great alternative to index and active mutual funds. They are liquid and actively trade on the exchange throughout the day.

As of now, very few plans offer ETFs. One of the main concerns for adding them to retirement plans is the timeliness of trade execution. Right now this problem is shifted to the fund managers who only issue end of day price once all trades are complete.

I expect that ETFs will become a more common choice as they grow in popularity and liquidity. Many small and mid-size companies that look for low-cost solutions can use them for them as an alternative to their for their workplace retirement plans.

Company stock

Many companies offer their stock as a matching contribution or profit sharing incentive in their employee 401k plan. Doing so aligns employees’ objectives with the company’s success. While this may have positive intentions, current or former employees run the risk of having a large concentrated position in their portfolios. Even if your company has a record of high returns, holding significant amounts of company stock creates substantial financial risk during periods of crisis because one is both employee and shareholder. Enron and Lehman Brothers are great examples of this danger. Being overinvested in your company shares can lead to simultaneous unemployment and depletion of retirement savings if the business fails.

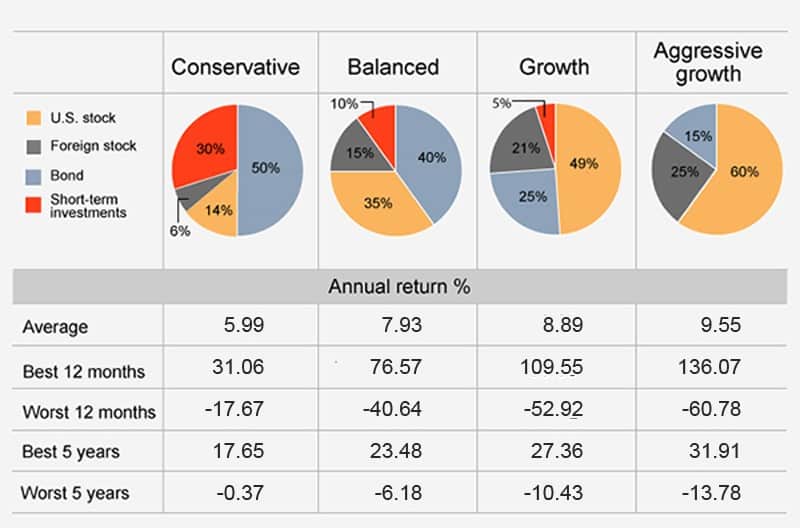

Allocation mix

You will most likely have a choice between a family of target retirement funds and a group of large-cap, mid-cap, small-cap, international developed, emerging markets stocks, a REIT, US government, corporate, high yield and international bond funds.

Your final selection should reflect your risk tolerance and financial goals. You should consider your age, family size, years to retirement, risk sensitivity, total wealth, saving and spending habits, significant future spending and so on.

You can use the table below as a high-level guidance.

Data source: Ibbotson Associates, 2016, (1926-2015). Past performance is no guarantee of future results. Returns include the reinvestment of dividends and other earnings. This chart is for illustrative purposes only. It is not possible to invest directly in an index. For information on the indexes used to construct this table, see footnote 1. The purpose of the target asset mixes is to show how target asset mixes may be created with different risk and return characteristics to help meet an investor’s goals. You should choose your investments based on your particular objectives and situation. Be sure to review your decisions periodically to make sure they are still consistent with your goals.

Source: https://www.fidelity.com/viewpoints/retirement/ira-portfolio?ccsource=email_monthly

Final recommendations

Here are some finals ideas how to make the best out of your 401k savings:

- At a minimum, you should set aside enough money in your 401k plan to take advantage of your employer’s matching contribution. It’s free money after all. However, the vesting usually comes with certain conditions. So definitely pay attention to these rules. They can be tricky.

- 2016 maximum contribution to 401k is $18,000 plus $6,000 for individuals over 50. If you can afford to set aside this amount, you will maximize the full potential of retirement savings.

- If your 401k plan is your only retirement saving, you need to have a broad diversification of your assets. Invest in a target retirement fund or mix of individual mutual funds to avoid concentration of your investments in one asset class or security.

- If your 401k plan is one of many retirement saving options – taxable account, real estate, saving accounts, annuity, Roth IRA, SEP-IRA, Rollover IRA or a prior employer’s 401k plan, you will need to have a holistic view of your assets in order to achieve a comprehensive and tax optimized asset allocation.

- Beware of hidden trading costs in your plan choices. Most no-load mutual funds will charge anywhere between 0.15% and 1.5% to manage your money. This fee will cover their management, administrative, research and trading costs. Some funds also charge upfront and backload fees. As you invest in those funds your purchase cost will be higher compared to no-load funds.

- If you hold large concentrated positions of your current or former employer’s stock, you need to mitigate your risk by diversifying the remainder of your portfolio.

If you have any questions about your existing investment portfolio or how to start investing for retirement and other financial goals, reach out to me at st****@***********th.com or +925-448-9880.

You can also visit our Insights page where you can find helpful articles and resources on how to make better financial and investment decisions.

About the author:

Stoyan Panayotov, CFA is the founder and CEO of Babylon Wealth Management, a fee-only investment advisory firm based in Walnut Creek, CA. Babylon Wealth Management offers personalized wealth management and financial planning services to individuals and families. To learn more visit our Private Client Services page here. Additionally, we offer Outsourced Chief Investment Officer services to professional advisors (RIAs), family offices, endowments, defined benefit plans, and other institutional clients. To find out more visit our OCIO page here.

Disclaimer: Past performance does not guarantee future performance. Nothing in this article should be construed as a solicitation or offer, or recommendation, to buy or sell any security. The content of this article is a sole opinion of the author and Babylon Wealth Management. The opinion and information provided are only valid at the time of publishing this article. Investing in these asset classes may not be appropriate for your investment portfolio. If you decide to invest in any of the instruments discussed in the posting, you have to consider your risk tolerance, investment objectives, asset allocation and overall financial situation. Different investors have different financial circumstances, and not all recommendations apply to everybody. Seek advice from your investment advisor before proceeding with any investment decisions. Various sources may provide different figures due to variations in methodology and timing,

Contact Us