Solving the student debt crisis

The looming student debt crisis

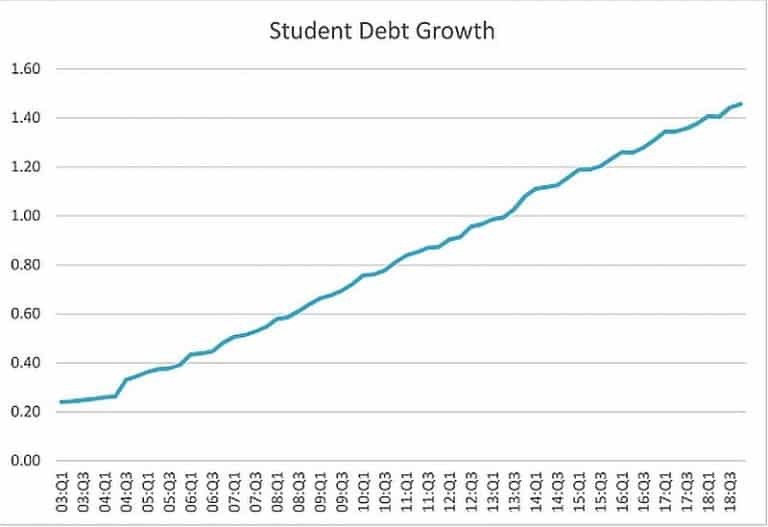

As a financial advisor working with many young families, I am regularly discussing college planning. Many of my clients want to help their children with the constantly growing college tuition. Currently, the amount of US student debt is $1.56 trillion, spread among 45 million borrowers. By 2023, 40% of borrowers can default on their loans. I am not running for president, but I am very curious about the upcoming debate about fighting the upcoming student debt in America.

One recent proposal from the Republican party was to allow 529 plan participants to pay off student debt.

Another proposal from the presidential candidate Elizabeth Warren is to cancel student debt partially or entirely for households based on their income. Furthermore, many Democrat candidates signed for free public college for all.

While all these ideas have certain merits, I am not confident that they will solve the problem long-term. As a parent and married to my wife who is paying off student loans, I would like to share my opinion. Here are some of my suggestions

Promote 529 plans

In one of my previous articles, I discussed the benefits of 529 plans. Sadly, only 30% of US families know about or use 529 plans. It’s really striking how little Americans know about this option. 529 plans are state-sponsored tax-advantaged investment accounts allowing parents and other family members to save for qualified college expenses. It literally takes 5-10 minutes to open a 529 account.

Make 529 contributions tax-deductible

Currently, 529 contributions are after taxes. The tax advantage comes from not paying taxes on any future capital gains if you use the funds to pay for eligible college expenses. Additionally, over 30 states offer full or partial state income tax deduction on 529 contributions.

I would like to go one step further and propose federal income tax deduction up to a certain annual limit (say $5,000 or $10,000) with a phaseout over certain household income level (call it $250,000). This income deduction will help low and middle-class families save for college without putting a massive strain on their budget.

Expand the Employer-sponsored 529 plans

In reality, most US families do not use the 529 plan because they don’t know about them or are uncertain about their investment choices. One way to popularize the 529 plan is motivating employers to include them as part of their benefits package similar to 401k plans. Employees can set up automatic payroll deposits and make regular contributions to their 529 accounts. Unfortunately, according to a recent survey by Gradadvisor, only 7% of employers offer 529 plans through their benefits.

Currently, the employer 529 match is taxable income to the parent. At the end of the year, the parent must pay personal taxes on any amount received through their employer.

I believe this provision is discouraging a lot of people to participate in these plans. In order to encourage higher participation in employer-sponsored 529 plans., the employer match should not be treated as income to the parent if used for qualified educational expenses.

Promote more work-study grants and employer-sponsored scholarships

Many college graduates leave school unprepared for the real world. Sometimes, I feel that there is a disconnect between skills learned at school and those needed to compete in the work marketplace.

While many public and private schools are doing a great job in teaching students those skills, I think we can do much better by connecting the school programs with the business. Let’s face it. Unless you are from an Ivy League school, how many students have had the chance to speak to a corporate CEO, a successful small business owner or a community leader.

With US unemployment at a record low, many businesses are struggling to find qualified workers. If we can encourage schools and employers to work together and set up employer-sponsored scholarships, internship programs, and work-study grants, we will have a lot more students learning real-life skills, earn money while study and potentially come out with smaller or no student loans.

Have personal finance as a mandatory class in high school and college

Only 1/3 of states require a mandatory personal finance class in high school. And zero states mandate it in college. It may sound radical, but I believe that every high school and public college should require one personal finance class in the curriculum regardless of the student major.

Teaching kids and young adults essential financial skills like saving money, budgeting, and investing will help them make better choices later in life.

It also means that we need to find teachers who can coach personal finance. Unfortunately, finance and economics are mostly taught in business schools and largely ignored outside of the space. This is where connecting schools with local business leaders can be helpful.

Extend the Non-Taxable Loan Forgiveness

There are several Federal and State programs that offer Loan Forgiveness. However, in most cases, student loan forgiveness is treated as taxable income in the year when the loan was written off. For some borrowers performing public service or working as teachers, lawyers and physicians in underserved areas, the loan forgiveness can be tax-free.

If your employer offers to pay off your student loans, you will receive a tax bill from the IRS. The amount of your forgiven loan will be added to your annual income and taxed as ordinary income. Knowing this tax trap, very few people opt for that option. If you can’t afford to pay off your student loan, what are the chances you can pay the taxes on the loan forgiveness?

Separately, being an elementary school teacher in a desirable area like Manhattan or San Francisco doesn’t make you financially better off than the rest of your colleagues. Most teachers can’t afford to live in San Francisco or Manhattan on a teacher’s salary, how do we expect them to pay off their loans.

Furthermore, non-taxable loan forgiveness should be designed to reward responsible borrowers who are paying off their loans regularly. I think a dollar to dollar match could encourage more people to pay off their loans.

What about loan cancellation

Canceling loans entirely or partially is a very admirable idea but it could turn into a double-edged sword. On one hand, it’s not completely fair to people who are diligently paying off their student loans month after month. And on the other hand, loan cancellation will encourage more people to take on student debt and not pay it. It might provide temporary relief, but it will not solve the problem long-term. I much rather find a way to empower and educate borrowers.

Improve student access to financial advice

How many parents or students speak to a financial advisor before taking a student loan? I bet a lot less than we hope for. Maybe it’s partially our fault as finance professionals but as a society, we need to find a way to get more financial advisors and colleges.

Before the TJCA of 2017, professional service expenses such as fees for CPAs and financial advisors were tax-deductible. I am not sure how many people took advantage of this deduction, probably not too many, but it was one way to encourage people to seek professional financial advice.

The sad truth is that the people who can afford financial advice are not those who needed it the most. So how about, make the financial advisory fees tax-deductible for low income and middle-class families. Or encourage financial advisors to provide free public service. I believe many of my colleagues will be happy to provide free advice in a meaningful and impactful way.

Reach out

If you’d like to discuss how to pay off your student loans, open a new 529 plan or make the most out of your existing 529 account, please feel free to reach out and learn more about my fee-only financial advisory services. I can meet you in one of our offices in San Francisco, Oakland, Walnut Creek, and Pleasant Hill areas or connect by phone. As a CFA® Charterholder with an MBA degree in Finance and 15+ years in the financial industry, I am ready to answer your questions.

Stoyan Panayotov, CFA

Founder | Babylon Wealth Management

Subscribe to get our new Insights delivered right to your inbox

Contact Us