End of Summer Market Review

End of Summer Market Review

Happy Labor Day!

Our hearts are with the people of Texas! I wish them to remain strong and resilient against the catastrophic damages of Hurricane Harvey. As someone who experienced Sandy, I can emphasize with their struggles and hope for a swift recovery.

I know that this newsletter has been long past due. However, as wise people say, it is better late than never.

It has been a wild year so far. Both Main and Wall Street kept us occupied in an electrifying thriller of election meddling scandals, health reforms, political battles, tax cuts, interest rate hikes and debt ceiling fights (that one still to unfold).

Between all that, the stock market is at an all-time high. S&P 500 is up 11.7% year-to-date. Dow Jones is up 12.8%, and NASDAQ is up to the whopping 24%. GDP growth went up by 3% in the second quarter of 2017. Unemployment is at a 10-year low. 4.3%.

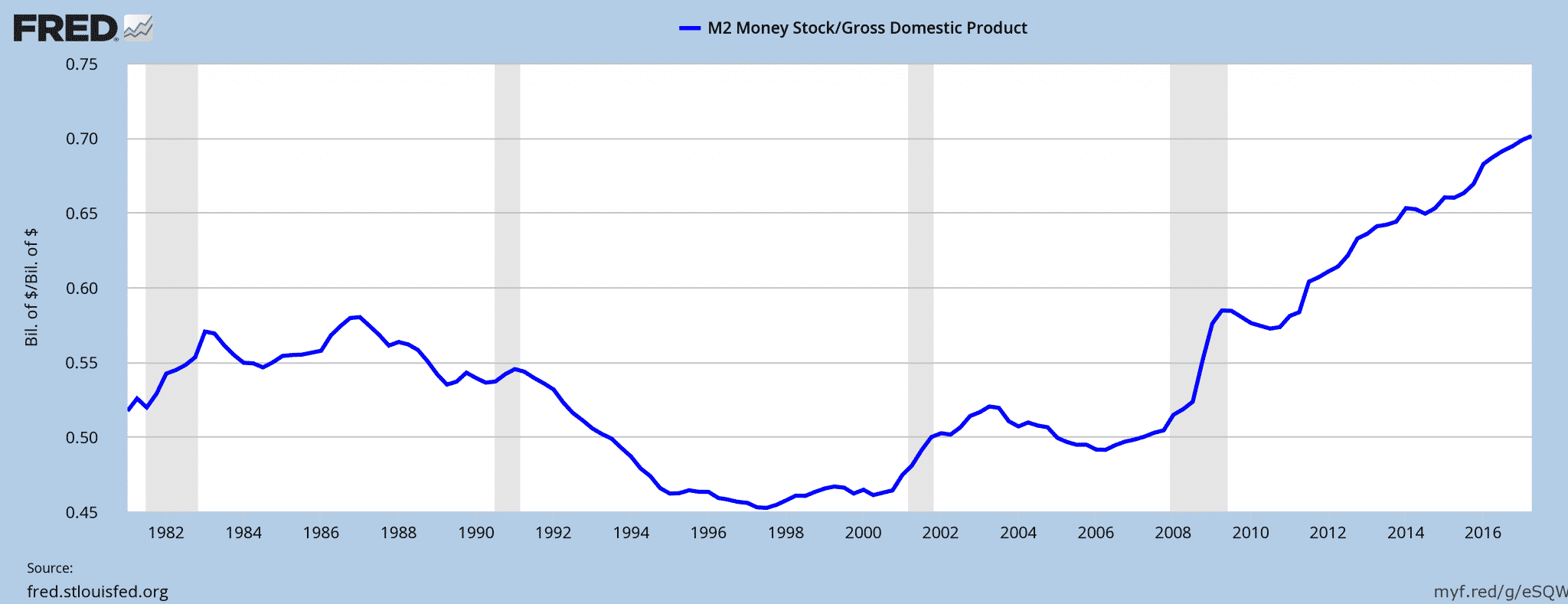

Moreover, despite record levels, very few Americans are feeling the joy of the market gains and feel optimistic about the future. US families are steadily sitting on the sideline and continuing to pile cash. As of June 2007, the amount of money in cash and time deposits (M2) was 70.1% of the GDP, an upward trend that has continued since the credit crisis in 2008.

Source: US Fed, https://fred.stlouisfed.org/graph/?g=dZn

Given that the same ratio of M2 as % of GDP is 251% in Japan, 193% in China, 91% in Germany, and 89% in the UK, US is still on the low end of the developed world. However, this is a persistent trend that can reshape the US economy for the years to come.

The Winners

This year’s rally was all about mega-cap and tech stocks. Among the biggest winners so far this year we have Apple (AAPL), up 42%, Amazon (AMZN), 27%, NVIDIA (NVDA), 54%, Adobe, 48%, PayPal, 55%. Netflix, 36%, and Visa (V), 33%,

Probably the biggest story out there is Amazon and its quest to disrupt the way Americans buy things. Despite years of fluctuating earnings, Amazon is still getting full support from its shareholders who believe in its long-term strategy. The recent acquisition of Whole Foods and announcement of price drops, only shows that Amazon is here to stay, and all the key retail players from Costco, Wall-Mart, Target, and Walgreens to Kroger’s, Home Depot, Blue Apron and AutoZone will have to adjust to the new reality and learn how to compete with Amazon.

The Laggards

Costco, Walgreens, and Target are bleeding from the Amazon effect as they reported- 0.49%, -0.74% and -21% year-to-date respectively. Their investors are become increasingly unresponsive to earnings surprises and massively punishing to earnings disappointments.

Starbucks, -0.74%, is still reviving itself after the departure of its long-time CEO, Howard Shultz, and will have to discover new revenue channels and jump-start its growth.

The energy giants, Chevron, -5%, Exxon, -12%, and Occidental Petroleum, -14.5% are still suffering from the low oil prices. With OPEC maintaining current production levels and surge in renewable energy, there is no light at the end of the tunnel. If these low levels continue, I will expect to see a wave of mergers and acquisitions in the sector. Those with a higher risk and yield appetite may want to look at some of the companies as they are paying a juicy dividend – Chevron, 4%, Exxon, 4%, and Occidental Petroleum, 5.4%

AT&T, -7% and Verizon, -5%, are coming out of big acquisitions, which down-the-road can potentially create new revenue channels and diversify away from the otherwise slow growing telecom business. In the near-term, they will continue to struggle in their effort to impress their investors. Currently, both companies are paying above average dividends, 5.15%, and 4.76%, respectively.

And finally, Wells Fargo, -4%. The bank is suffering from the account opening scandals last year and the departure of its CEO. The stock has lagged its peers, which reported on average, 8% gains this year. While the long-term outlook remains positive, the short-term prospect remains uncertain.

Small Caps

Small Cap stocks as an asset class have not participated in this year’s market rally. Despite spectacular 2016 returns, small cap stocks have remained in the shadow of the uncertainty of the expected tax cuts and infrastructure program expansion. While I believe the Congress will come out with some tax reductions in the near term, the exact magnitude is still unclear. My long-term view of US small caps remains bullish with some near-term headwinds.

International Stocks

After several years of lagging behind US equity markets, international stocks are finally starting to catch up. The Eurozone reported 2% growth in GDP. MSCI EAFE is up 17.5% YTD, and MSCI Emerging Markets is up 28% YTD.

Despite the recent growth, International Developed and Emerging Market stocks remain cheap on a relative basis compared to US Stocks. I maintain a long-term bullish view on international and EM stocks with some caution in the short-term.

Even though European Central Bank has kept the interest rates unchanged, I believe that its quantitative easing program will slow down towards the end of 2017 and beginning of 2018. The German bund rates will gradually rise above the negative levels. The EUR / USD will breach and remain above 1.20, a level not seen since 2014.

Interest Rates

I am expecting maximum one or may be even zero additional rate hikes this year. Under Janet Yellen, the Fed will continue to make extremely cautious and well-measured steps in raising short term rates and slowing down of its Quantitative Easing program. Bear in mind that the Fed has not achieved its 2% inflation target and any sharp rate hikes can ruin the already fragile balance in the fixed income space.

Real Estate

After eight years of undisrupted growth, US Real Estate has finally shown some signs of slow down. While demand for Real Estate in the primary markets like California and New York is still high, I expect to see some cooling off and normalization of year-over-year price growth

US REITs have reported 3.5% total return year-to-date, which is roughly the equivalent of -0.5% in price return and 4% in dividend yield.

Some retail REITs will continue to struggle in the near-term due to store closures and pressure from online retailers. I encourage investors to maintain a diversified REIT portfolio with a focus on strong management, sustainability of dividends and long-term growth prospects.

Gold

After several years of underperformance, Gold is making a quiet comeback. Gold was up 8% in 2016 and 14% year-to-date. Increasing market and political uncertainty and fear of inflation are driving many investors to safe havens such as gold. Traditionally, as an asset class, Gold has a minimal correlation to equities and fixed income. As such, I support a 1% to 5% exposure to Gold in a broadly diversified portfolio as a way to reduce long-term risk.

About the author: Stoyan Panayotov, CFA is a fee-only investment advisor based in Walnut Creek, CA. His firm Babylon Wealth Management offers fiduciary investment management and financial planning services to individuals and families.

Disclaimer: Past performance does not guarantee future performance. Nothing in this article should be construed as a solicitation or offer, or recommendation, to buy or sell any security. The content of this article is a sole opinion of the author and Babylon Wealth Management. The opinion and information provided are only valid at the time of publishing this article. Investing in these asset classes may not be appropriate for your investment portfolio. If you decide to invest in any of the instruments discussed in the posting, you have to consider your risk tolerance, investment objectives, asset allocation and overall financial situation. Different investors have different financial circumstances, and not all recommendations apply to everybody. Seek advice from your investment advisor before proceeding with any investment decisions. Various sources may provide different figures due to variations in methodology and timing,

Contact Us