The Rise of Momentum Investing

The Rise of Momentum Investing

While the momentum theory has been around for two decades, we had to wait until 2017 to see the rise of momentum investing. The largest momentum ETF (MTUM) is up 35% YTD. And unless something dramatic happens in the remaining few weeks, momentum will crush all major market-cap weighted indices and ETFs.

About this time last year, I posted my first article about momentum investing in Seeking Alpha. You can see my article here. At that time MTUM had only $1.8 billion of AUM and trailed the S&P 500 2016 returns in the range of 5% versus 12%. Eleven months later, MTUM is up 35% versus 16.5%. I can’t take any credit for calling this wide margin in performance, but it certainly grabbed the attention of investors. MTUM is currently at $4.8b AUM and possibly growing even more down the road.

Learn more about our Private Wealth Management services

What is momentum investing

So what is momentum and why do we keep hearing about it a lot more lately?

The momentum investing is a pure behavioral play. Not surprisingly the rise of momentum investing coincided with Richard Thaler’s Nobel award for his work on how human behavior and finance play out together.

Momentum investing exploits the theory that recent stock winners will continue to rise in the near-term. The strategy is based on the 1993 Journal of Finance research “Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency” by Narasimhan Jegadeesh and Sheridan Titman

Their research discovers a pattern that buying stocks that have performed well in the past and selling stocks that have performed poorly generate significant positive returns over 3- to 12-month holding periods. Furthermore, the research discusses that the success of this strategy is due to behavioral finance factors.

Investors commonly overact on the news and therefore overbuy the winners and oversell the losers.

Many investors consider the momentum strategy as a substitute for growth investing. However, the momentum theory embraces both value and growth stocks as long as they have risen in the past 6 to 12 months.

While the momentum theory has been around for over 20 years, the strategy has not received a wide acceptance amongst investors. Despite its academic fundamentals, momentum strategy has experienced contradictory practical interpretations amongst fund managers, which has reported a massive variability of returns.

Fortunately, the growing popularity of market-cap and smart beta ETFs made the momentum strategy widely available to retail investors. Further down, I will discuss how to take advantage of the momentum theory by using MTUM – iShares Edge MSCI USA Momentum Factor ETF. This ETF has been around since April 2013. It has a dividend yield of 1.12% and an expense ratio of 0.15%.

MTUM replicates the MSCI USA Momentum Index. MSCI USA Momentum Index uses a multi-step process to filter for stocks that fit the momentum criteria. The composition process starts with selecting companies with the highest 6- and 12- month performance. The performance is later weighted by their 3-year standard deviation and given a momentum score. The final weight in the momentum index is given by multiplying the momentum score by the market capitalization weight in the parent index. In this case, the parent index is MSCI USA Index, which has 616 constituents and covers about 85% of the US market cap. Company weights for MSCI USA Momentum Index are capped at 5%. The index is rebalanced semiannually. However, spikes in market volatility can trigger ad-hoc rebalancing.

Performance and risk

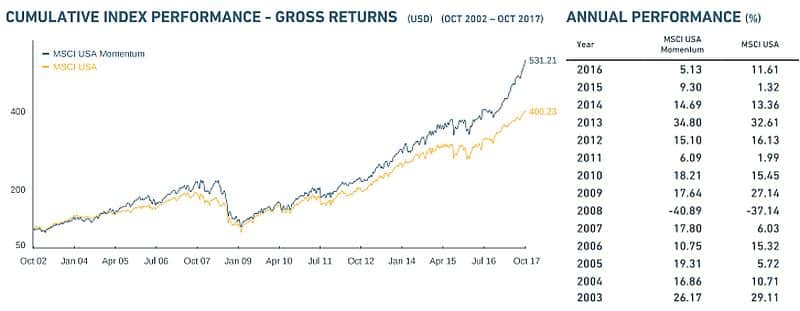

MSCI USA Momentum Index has consistently outperformed MSCI USA and S&P 500 since its inception. The index has achieved a cumulative return of 531% versus 400% for MSCI USA and 423% for S&P 500 since October 2002.

In annualized terms, MSCI USA Momentum Index posted 9.07% 10-year return and 13.65% return since its inception in 1994.

The index beat its parent in 9 out of the past 15 years and underperformed in six – 2003, 2006, 2008, 2009, 2012 and 2016.

It is an interesting observation that the Momentum strategy underperformed in the years following a significant market pullback or sluggish return (02-03, 05-06, 08-09 and 11-12). It takes a two-year cycle for the Momentum Index to start outperforming again after experiencing a negative period. The composition of the index is somewhat reactive, which naturally doesn’t allow it to take advantage of market rallies in specific sectors.

Source: MSCI

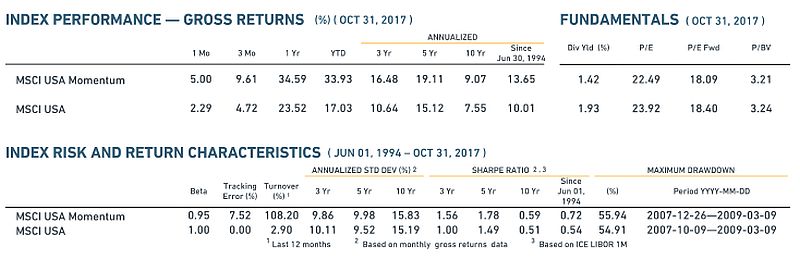

Counterintuitively to what some may think, the MSCI Momentum Index has reported lower standard deviation (risk) than its parent index for the past 3-year and slightly higher standard deviation for the 5- and 10-year period. The risk-weighted methodology described earlier helps the index cap its volatility despite high turnover.

Higher returns and capped volatility has allowed the momentum index to report consistently high risk-adjusted returns. Its 10-year Sharpe ratio is 0.59 versus 0.51 for MSCI USA and 0.53 for S&P 500. Since inception, the Momentum Index posted the impressive 0.72 versus 0.54 MSCI USA and S&P 500.

Source: MSCI

MTUM ETF

Going back to the iShares Edge MSCI USA Momentum Factor ETF, it has been around since April 2013. Since inception, its performance has been consistent with the index. MTUM posted 17.3% return versus 13.4% for S&P 500 and 15.32% for IWF, Russell 1000 growth ETF.

MTUM has reported a Sharpe ratio of 1.61 vs. 1.33 for S&P 500 and 1.41 for IWF.

Few other interesting facts for investors looking to diversify. The US market correlation is equal to 0.87. Beta is 0.90. Alpha is 4.7%, and R2 is 73.7%. In other words, the momentum strategy achieved its return not only with less risk but a lot lower correlation to the total market, which is critical for portfolio diversification.

MTUM Holdings

Momentum investing is a dynamic strategy with quarterly rebalancing. Due to its 114% turnover, it is extremely cost ineffective for the average retail investor to replicate it

Currently, MTUM overweights Financials, Technology, and Industrials which have primarily driven the market since the beginning of 2017. Simultaneously, the ETF underweights Consumer Cyclical, Utilities, and Energy. Its main holdings include Microsoft, Bank of America, JP Morgan, Apple, United Health Group, NVIDIA, Home Depot, Comcast, and Boeing. Just to illustrate the dynamic nature of this strategy, a year ago its top holdings were in Technology and Utilities with leading names such as Facebook, Amazon, Google, and Nextera.

Final thoughts

- The momentum strategy has outperformed the broad market in the past 22 years.

- While being in the public eye for over two decades and posting impressive long-term absolute and risk-adjusted returns, the momentum strategy is still not a highly popular trade and has mostly been a theoretical exercise with conflicting practical results.

- Only lately, the rise of ETFs had made the strategy available to regular investors.

- The momentum strategy tends to lean towards sectors with a recent high

- Like any factor strategy, the momentum can underperform the broad market for extended periods

About the author: Stoyan Panayotov, CFA is the founder and CEO of Babylon Wealth Management, a fee-only investment advisory firm. Babylon Wealth Management offers highly customized Outsourced Chief Investment Officer services to professional advisors (RIAs), family offices, endowments, defined benefit plans and other institutional clients. To learn more visit our OCIO page here.

Holdings disclaimer: I own MTUM and we regularly invest MTUM for our clients.

Disclaimer: Past performance does not guarantee future performance. Nothing in this article should be construed as a solicitation or offer, or recommendation, to buy or sell any security. The content of this article is a sole opinion of the author and Babylon Wealth Management. The opinion and information provided are only valid at the time of publishing this article. Investing in these asset classes may not be appropriate for your investment portfolio. If you decide to invest in any of the instruments discussed in the posting, you have to consider your risk tolerance, investment objectives, asset allocation and overall financial situation. Different investors have different financial circumstances, and not all recommendations apply to everybody. Seek advice from your investment advisor before proceeding with any investment decisions. Various sources may provide different figures due to variations in methodology and timing,

Contact Us